China’s Post-2005 Generation Beauty Consumers: The Next Growth Engine for Beauty Brands

- See Qian

- 3 days ago

- 5 min read

China’s beauty market is entering a new growth cycle, and post-2005 consumers are becoming one of its most important emerging audiences. Young, digitally fluent, value-conscious, and highly influenced by content, this generation is already changing how beauty products are discovered, evaluated, and purchased.

A Young Consumer Group With Long-Term Market Potential

Post-2005 consumers are moving from “future potential” into active beauty consumption. According to the report, China’s 18–21-year-old post-2005 population reached approximately 56.91 million by the end of 2020, representing 4.04% of the total population. As this group enters university, internships, and early employment, beauty spending is expected to become more regular and more self-directed.

The commercial scale is already meaningful:

China’s total cosmetics retail market is estimated at RMB 822.5 billion in 2025.

Post-2005 beauty consumption accounts for a theoretical 7.55% share.

Under the neutral scenario, the post-2005 beauty market reaches RMB 62.1 billion in 2025.

By 2030, the segment could exceed RMB 109.4 billion under the neutral scenario.

This makes the post-2005 audience more than a youth marketing target. It is a long-term growth pool for China beauty brands, skincare companies, colour cosmetics players, and content commerce platforms.

Beauty Decisions Are Moving From Search-First to Content-Triggered

Post-2005 consumers do not make beauty decisions through a single channel. Content creates interest, search validates the product, and social proof reduces purchase hesitation. This makes the decision journey more fluid, but also more demanding for brands.

The report shows that 51.35% of post-2005 consumers still follow a search-first behaviour, while 37.84% follow a “see content → search to verify → purchase” path. This means short videos, livestreams, creator content, and social posts can trigger demand, but they do not replace verification.

For beauty marketers, the key lesson is clear: visibility must connect to trust. A product that appears in content must also be easy to search, easy to compare, easy to understand, and easy to buy. SEO, Xiaohongshu content, Douyin videos, product pages, reviews, and livestreaming should work as one connected conversion journey.

Value Matters, But Cheap Alone Will Not Win

Post-2005 beauty consumers are highly exposed to trends, but many are still at an early stage of financial independence. This creates a strong value mindset. They want products that feel affordable, but they are not simply choosing the lowest price.

The audience profile explains this clearly:

Women account for 86.49% of the post-2005 beauty consumer sample.

First-tier, new first-tier, and second-tier cities together account for more than 73.78%.

66.22% rely mainly on family support.

50% have monthly disposable income of RMB 1,500–3,000.

This creates a practical beauty mindset. Post-2005 consumers want products that are accessible, safe, effective, and easy to justify. For brands, the strongest proposition is not “cheap beauty”. It is credible value: clear ingredients, proven benefits, trusted reviews, and pricing that fits student and early-career budgets.

Functional Skincare Is the Core Growth Opportunity

Skincare is the clearest entry point into this generation’s beauty routine. Post-2005 consumers are still building daily habits, but their expectations are already sophisticated. They are not only buying basic products; they are looking for solutions to specific skin concerns.

Key category demand includes:

81.08% select basic skincare.

71.62% select functional skincare.

60.81% select colour cosmetics.

Their strongest skincare needs are also highly practical. Brightening and evening skin tone leads at 72.97%, followed by oil control and acne care at 55.41%. Barrier repair, soothing, and hydration each stand at 52.70%.

This points to a strong innovation direction: mild daily efficacy. Products need to be gentle enough for frequent use, effective enough to show visible results, and simple enough for young consumers to understand quickly.

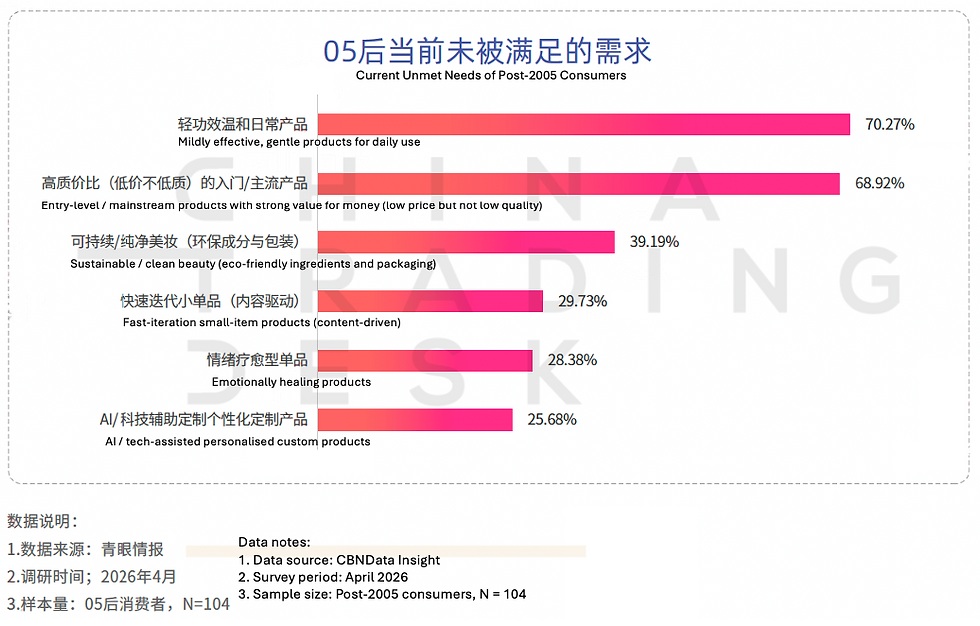

Product Pain Points Create Clear Innovation Space

Post-2005 consumers are showing clear gaps in product performance, safety confidence, and value for money. Their biggest frustrations are concentrated around makeup longevity, ingredient transparency, sensitive-skin repair, slow or unclear efficacy, and products that feel too expensive for their budgets.

The main pain points include:

Makeup performance: 75.68% are concerned about products that do not last.

Ingredient trust: 74.33% worry about unclear ingredients or safety.

Gentle efficacy: 72.98% want mild products with daily visible benefits.

Value for money: 67.57% seek affordable entry-level or mainstream products.

In short, brands should focus less on overcomplicated claims and more on products that are gentle, reliable, clearly explained, and easy for young consumers to justify buying.

Everyday Scenarios Are Shaping Beauty Demand

Post-2005 beauty consumption is closely tied to daily life. These consumers are not only buying for special occasions or online self-expression. They are buying for school, commuting, social moments, photos, outdoor activities, and quick touch-ups.

The report identifies daily commuting and school as the leading usage scenario at 78.38%, followed by social and dating occasions at 75.68%. This means beauty products need to perform in real-life conditions: long hours, changing weather, public transport, classrooms, cafés, and social settings.

For brands, scenario-based communication will matter more. A “long-lasting” claim becomes stronger when shown through a school day or commute. A “soothing” claim becomes more persuasive when connected to stressed skin after makeup, sun exposure, or late nights. The more relatable the scenario, the easier it is for young consumers to imagine the product in their own routine.

Four Key Post-2005 Beauty Consumer Types

Post-2005 beauty consumers are shaped by four main motivations: ingredient trust, self-reward, value for money, and social expression.

Rational Ingredient Seekers — 67.57%

Focus on ingredients, efficacy, and visible results. They prefer products with clear claims, transparent formulas, and real user proof.

Emotional Self-Reward Consumers — 54.05%

See beauty as part of self-care and personal enjoyment. They respond to products with ritual value, pleasant textures, attractive packaging, and lifestyle storytelling.

Value-Savvy Consumers — 51.35%

Look for affordable beauty products that feel safe, effective, and worth the price. Entry-level skincare and mainstream products are especially relevant to this group.

Community Expression Consumers — 13.51%

Use beauty to express identity, follow trends, and join social conversations. This group is smaller, but important for content sharing and brand buzz.

Overall, China’s post-2005 beauty consumers are mainly driven by credible efficacy and ingredient trust, supported by value, emotional appeal, and content-friendly identity expression.

What Beauty Brands Should Do Next

To win post-2005 consumers, beauty brands need a connected strategy across product, content, search, and commerce.

Priority actions include:

Build trust through ingredient transparency and easy-to-understand efficacy education.

Use content to trigger demand, but make search verification simple.

Show products in real daily scenarios, not only polished campaign visuals.

Prioritise mild functional skincare and long-wear daily makeup.

Create affordable entry products that still feel credible and desirable.

Strengthen reviews, user-generated content, and creator proof.

Connect SEO, social content, livestreaming, and product pages into one purchase journey.

Final Takeaway

Post-2005 generation consumers are already reshaping China’s beauty market. They are content-led, but not easily persuaded. They are value-conscious, but not purely price-driven. They want beauty products that are effective, safe, affordable, and relevant to everyday life.

The brands best placed to win will be those that close the trust gap. In China’s next beauty growth cycle, functional skincare, transparent proof, content-native communication, and high value-for-money products will define the strongest route to post-2005 consumer growth.

Comments